Windstory #11 - Everything we can learn from the French floating wind auction

The French Energy Regulatory Commission (CRE) has published a detailed report on the latest floating wind auctions. We analyze the key points.

Hello everyone and welcome to a new issue of Windstory, the article section of Windletter. I'm Sergio Fernández Munguía (@Sergio_FerMun) and here we discuss the latest news in the wind power sector from a different perspective. If you enjoy the newsletter and are not subscribed, you can do so here.

Windletter is sponsored by:

🔹 Tetrace. Specialized services in operation and maintenance, engineering, supervision, inspection, technical assistance, and distribution of spare parts in the wind sector. More information here.

🔹 RenerCycle. Development and commercialization of solutions and specialized services in the circular economy for renewable energies, including comprehensive dismantling of wind farms and waste management, refurbishment and sale of components and wind turbines, management and recycling of blades and others. More information here.

Windletter está disponible en español aquí

Windstory is the articles section of Windletter, where we publish single-topic articles and share interesting stories from the wind energy sector.

From time to time, without a set schedule, a new edition of Windstory will arrive in your inbox.

🌊 Everything we can learn from the French floating wind auction

Last December, France awarded two floating wind blocks ranging between 230 and 280 MW in the so-called AO6 auction. The winners were the Narbonaise project, owned 50% by Ocean Winds and Banque des Territoires, and the Golfe de Fos project, owned 50% by EDF and Maple Power.

Now, thanks to a comprehensive report by the French Energy Regulatory Commission (CRE), we can learn many interesting details about the auction in an anonymized manner. The published information is based on the documentation submitted by developers to participate in the process, and I believe it is a great exercise in transparency from which much can be learned.

💰 Economic data

The awarded prices for the winners were a CfD of €92.70/MWh and €85.90/MWh for 20 years, respectively—very competitive considering this is floating wind. Moreover, we know that the winning developers were not particularly cheap or reckless, as the average bid price was €106.29/MWh and €103.24/MWh, respectively, indicating strong competition.

Other relevant financial data published by the CRE:

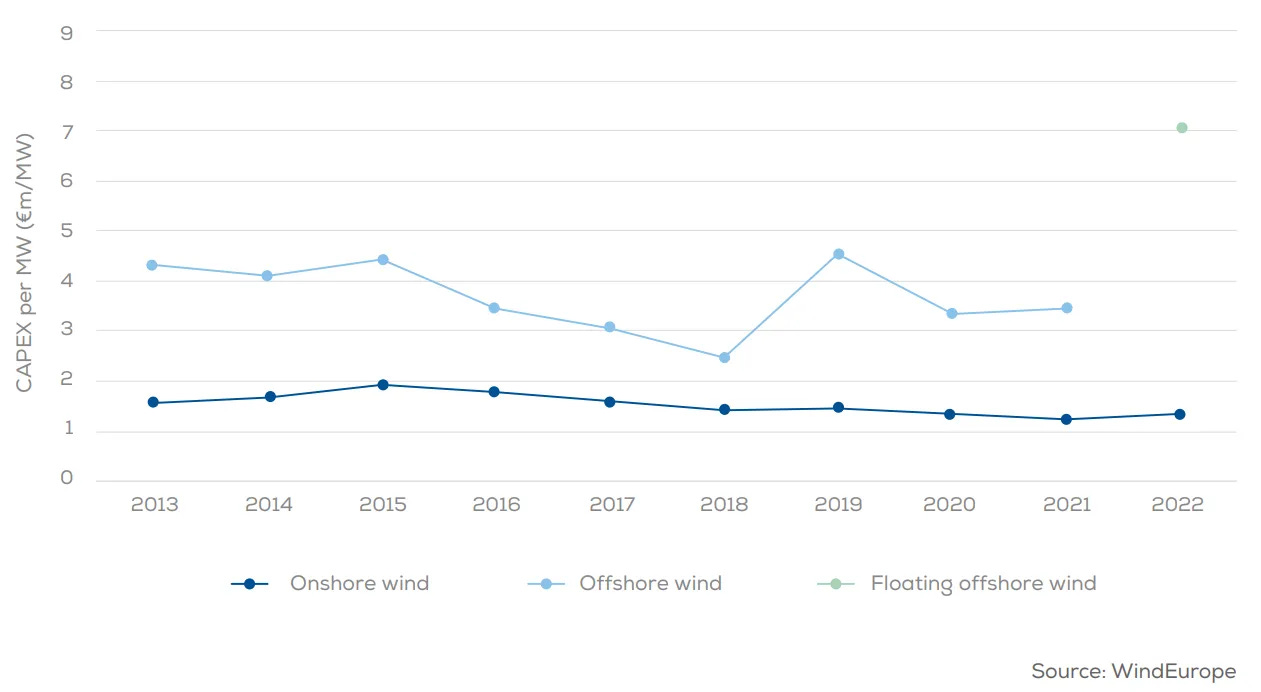

CAPEX (Investment cost): Between €3.2 and €4.2 million per installed MW.

OPEX (Operation and maintenance costs): Between €58,000 and €82,000/MW/year.

It is quite surprising that the CAPEX values per installed MW are so contained and closely aligned with the costs of fixed-bottom offshore wind. Below, I’ve included the latest data published by WindEurope (up to 2022).

Is the technology mature enough, or is this an excess of optimism from the developers?

The CRE is not entirely convinced, as its report states that four bids were reviewed due to a potential risk that actual costs might be higher, making the project unviable. However, they also point out that no bids were disqualified because the projects have room for redesign, and contractual penalties discourage potential withdrawals.

🔧 Will the installed turbines come from Chinese OEMs?

Focusing now on technology, according to the CRE's analysis, the proposals include turbines from Vestas, Siemens Gamesa, and GE Vernova, as well as Chinese manufacturers like Dongfang, Mingyang, Goldwind, and CSSC. It’s important to note that bidders are not required to select a specific manufacturer but must propose one (likely several).

Apparently, the CRE assesses the technological maturity of the proposed turbines. If a manufacturer presents a model that is still at the prototype stage or lacks references in commercial wind farms, it may negatively impact the technical feasibility evaluation. However, technical and financial robustness only carries a weight of 5 points in the evaluation criteria, while price accounts for 70%, environmental approach 13%, and social impact and territorial development 12%.

On the other hand, the CRE has also stated that some bids include turbines with capacities and sizes larger than those currently available commercially in Europe. And this is in the context of floating wind, which presents an additional technical challenge compared to fixed-bottom wind.

For example, some projects consider turbines with a unit capacity of 22.6 MW, which would align with the Siemens Gamesa 21+ MW model, but this is not a commercially available model at the moment.

Since the projects will be commissioned between August 2031 and February 2032, this would imply that SGRE will have a commercially available floating version by then. It may seem like a long time, but contracts will need to be signed at least around three years in advance.

Of course, another possibility is that these could be Chinese turbines from one of the mentioned manufacturers, but the reality is that these models are also currently under development and have no proven track record in Europe.

To reduce uncertainty and score higher on the technical evaluation, developers have submitted letters of support from manufacturers stating the commercial availability of these models by the time the wind farms are commissioned.

However, we also know that Western manufacturers are reluctant to continue increasing turbine sizes. And while SGRE is installing a 21+ MW prototype, it has kept the project as low profile as possible and has yet to make any public statements about it.

⚓ And what about the floating structures?

Another interesting point is that there is absolutely no mention of floating structure selection or its potential technical risks. This is likely because it is much harder to evaluate, given that the technology is far less mature.

What we do know is that the EDF and Maple Power consortium is highly likely to use structures from the French company BW Ideol, with whom they have had an agreement since 2022.

BW Ideol’s proposal is based on concrete, allowing for a high level of local manufacturing and avoiding dependence on large shipyards for production.

That said, I would like to see a port with enough space to manufacture 20-30 units. The ones in the photo below are the structures for the Eolmed pilot wind farm, featuring Vestas V164-10.0 MW turbines, which are currently in the assembly process.

Besides the project in the photo, BW Ideol’s platform has been in operation since 2018 with two prototypes in France and Japan. The company recently announced an updated design to accommodate 15 MW+ turbines.

📌 Conclusions

The main takeaway is that the AO6 auction has been competitive and clearly reflects the progress of floating wind technology.

However, financial and technological risks remain. Developers must ensure project viability in terms of profitability, and OEMs and floating structure suppliers must be able to deliver a mature and reliable product.

And what do you think?

Thank you very much for reading Windletter and many thanks to Tetrace and RenerCycle, our main sponsors, for making it possible. If you liked it:

Give it a ❤️

Share it on WhatsApp with this link

And if you feel like it, recommend Windletter to help me grow 🚀

See you next time!

Disclaimer: The opinions presented in Windletter are mine and do not necessarily reflect the views of my employer.