Windletter #136 - A push for repowering in Spain

Also: offshore turbine prices have risen, TotalEnergies inaugurates a hybridized, off-grid wind farm, DNV and GE Vernova collaborate to improve blade reliability, and more.

Hello everyone and welcome to a new issue of Windletter. I'm Sergio Fernández Munguía (@Sergio_FerMun) and here we discuss the latest news in the wind power sector from a different perspective. If you're not subscribed to the newsletter, you can do so here.

Windletter is sponsored by:

🔹 Tetrace. Reference provider of O&M services, engineering, supervision, and spare parts in the renewable energy market. More information here.

🔹 RenerCycle. Development and commercialization of specialized circular economy solutions and services for renewable energies. More information here.

🔹 Nabrawind. Design, development, manufacturing, and commercialization of advanced wind technologies. More information here.

🔹 Ingeteam Wind Energy. A global technology and services partner for the wind energy industry, working with OEMs, utilities and asset owners. Find out more here.

Windletter está disponible en español aquí

The most read items from the last edition were: the video of the transport of the Vestas V172 at Tâmega, the concrete floating turbine WHEEL, and Nabrawind presenting Skylift.

Forgive me for taking so long since the last news edition, but the past few weeks have been a bit complicated work-wise, with some business trips that threw my routine off quite a bit, on top of the duties of a (still) trainee dad.

That said, let’s get to this week’s news.

Windletter is a publication supported by its community of readers. If you enjoy the content and want to be part of this community, you can subscribe for free or join as a paid subscriber to support the publication.

A push for repowering in Spain

MITECO, through IDAE, has published the provisional resolution proposal of the second call of its repowering programme, REPOTEN 2. In total, 80 wind repowering projects that will take €462 million, following a budget increase of €220 million to meet the strong demand.

Galicia takes the lion’s share (31.5% of the allocated capacity), followed by Andalusia (20.2%) and Castilla y León (15.4%). The projects must be completed before 30 June 2030 and were selected through competitive bidding, taking into account criteria such as: reduction of the aid requested, administrative viability, contribution to the electricity system (grid forming or storage), Just Transition initiatives, and reinforcement of the national and European value chain.

For anyone who wants to break down the technical data of the allocations, I recommend the excellent analysis by Kiko Maza, who has dissected the call like no one else. The main figures are:

2,387 MW of capacity after repowering.

1,879 MWh of associated storage.

€3,545M of eligible investment.

An average aid of €194k/MW.

A mix of technologies to be decommissioned, with Gamesa G4X and G5X turbines featuring prominently, plenty of Ecotecnia units, and some other slightly more “unexpected” models.

For a market like Spain, this is a very significant volume of capacity. To put the figure in perspective, 1,411.4 MW of wind were installed in 2025 and 1,186 MW in 2024. So this aid mobilizes a lot of megawatts for the years ahead.

On the other hand, a good share of the projects incorporate storage. However, it’s worth reading the fine print, because the real storage capacity is limited. The vast majority of projects, 57 of the 80, hybridize with very low-capacity storage, around 0.5 equivalent hours (1,760 MW and 927 MWh).

As Jorge Nevado rightly points out, in most cases this storage is a complement to manage imbalances, reduce some curtailment (present and future), participate in balancing services and, at most, optimize the market value of a small part of the generation. And of course, to score better in the tender 🙂

All in on repowering?

Looking at the results, it’s clear that Repoten 2 is a very good initiative to energize the sector. It modernizes one of the oldest fleets in Europe and allocates the aid based on criteria that aren’t purely economic, as has been requested from various quarters for a long time. On top of that, it’s a tool that will mobilize significant investment over the coming years.

But it deserves some reflection. Aren’t we betting too much on the sector’s activity coming mainly through this route in the years ahead?

Repowering is necessary and a great opportunity to modernize old wind farms and make better use of existing sites, but it should be compatible with the development of new greenfield capacity. An activity that is currently fairly stalled.

What about new grid access capacity? There are no nodes left with available capacity to connect new wind farms.

What about the never-ending capacity tenders? There are many nodes the Ministry has reserved for capacity tenders, where developers will compete for grid access. However, except for a few Just Transition tenders where coal plants have been closed, nothing else has been mobilized.

Or do we only aspire to replace what already exists?

If you want to read about repowering, I recommend some topics we’ve covered in Windletter before:

The potential of repowering, in data: the figures on the potential of repowering in Europe.

The numbers behind Iberdrola’s repowering projects: a specific case, with figures, from a large developer.

Reinforcing a foundation for partial repowering: the technical challenge of reusing the existing foundation.

Soft repowering: replacing the nacelle with one from another manufacturer: a less well-known modernization route.

When repowering doesn’t pay off: the case of Australia’s oldest wind farm, which won’t be repowered.

In addition, together with our sponsor RenerCycle, we recently visited the dismantling works of a real project.

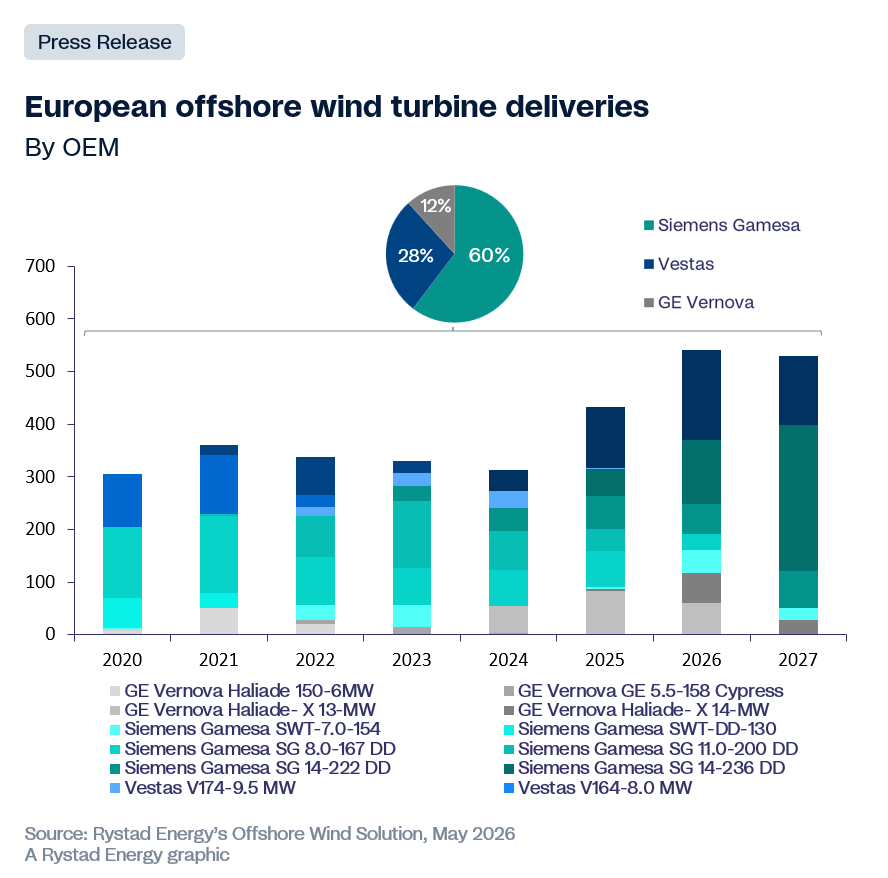

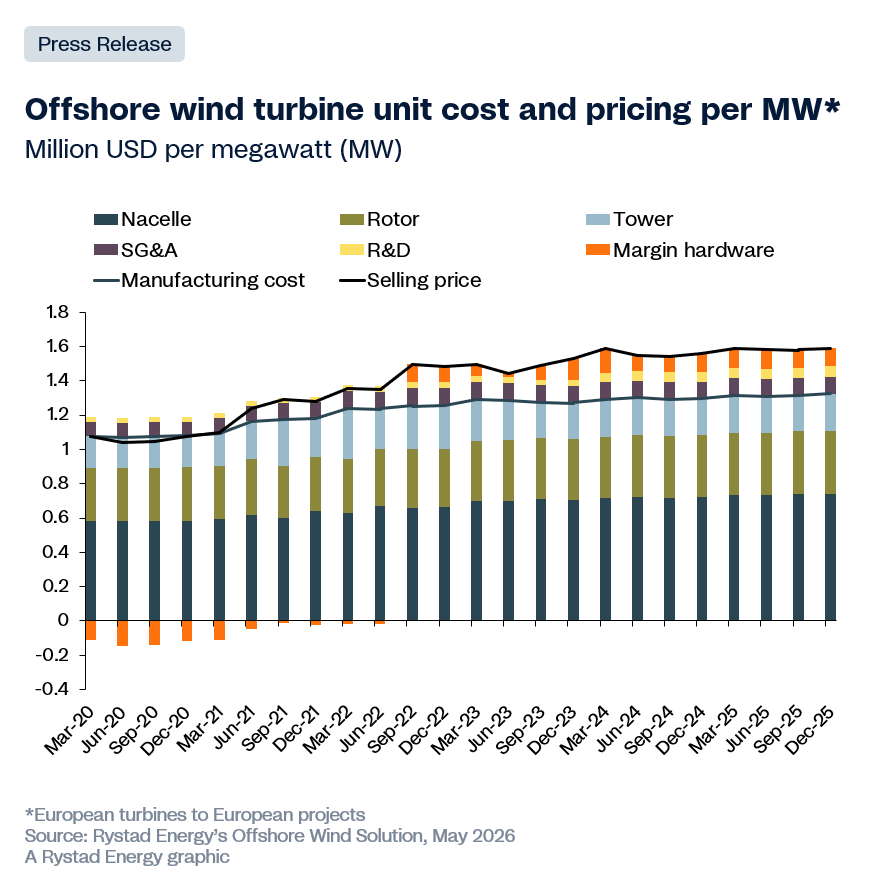

🌊 Offshore turbine prices have reportedly risen by 40-45%

According to an analysis by Rystad Energy, the sale prices of offshore wind turbines have reportedly increased by between 40% and 45% since 2020, far above the rise in manufacturing costs, which would sit at 20-25% over the same period.

The explanation Rystad points to is not just inflation, which has admittedly had a significant impact on the sector, but market concentration. With GE Vernova out of the offshore new-order business and no plans to return, Siemens Gamesa and Vestas share all of the orders from European developers. That lack of alternatives gives the OEMs pricing power and the ability to choose which projects they supply.

The bottleneck is not the same across all turbine components. It concentrates in the nacelles and blades, precisely where subcontracting the manufacturing is most difficult. Even so, we’ve already seen how Vestas leans on Aeolon for the supply of part of its blades.

Another relevant market change Rystad Energy highlights is who bears the risk. Between 2021 and 2023 the OEMs were trapped in fixed-price contracts and absorbed the cost increases through their margins. In the new contracts from 2023 onward, prices rose and part of the risk shifted to developers.

A few weeks ago we also noted that in onshore, Western prices have also risen by close to 45% since 2020, in a clear decision by the OEMs to recover margins rather than grow volume.

Is this situation sustainable in the medium and long term? Do the project economics still add up? Will these prices make developers look at China with different eyes?

🏭 Sany negotiates to build Egypt’s first wind turbine factory

The Chinese group Sany would be in advanced talks to build what would be Egypt’s first wind turbine factory.

Sany recently presented its plans at a meeting in Cairo with the Minister of Electricity and Renewable Energy. According to the ministry’s statement, there was talk of transferring and localizing the company’s technology and of executing 2,000 MW of projects. Neither the cost nor the location has been disclosed.

Egypt currently has around 3 GW of installed wind and aims for renewables to make up 42% of its mix by 2030. Historically it has been a market for Western OEMs, strongly led by SGRE, but in recent years the Chinese have positioned themselves.

Goldwind has 650 MW operating in the Gulf of Suez (one of the areas with the best onshore wind resource in the world) and Envision has announced a 1.1 GW contract. Siemens Gamesa, with more than 1.5 GW in the country, is also negotiating the 500 MW NIAT project.

What stands out is the openness of the Chinese OEMs to announcing factories outside China. It’s not just about selling turbines, but about manufacturing them locally in exchange for securing a guaranteed volume of 2,000 MW.

The question is whether those factories are sustainable in the long term, or are simply strategies to gain market share.

🔋 TotalEnergies inaugurates a hybridized, off-grid wind farm in Tierra del Fuego (Argentina)

TotalEnergies has commissioned a small wind farm in the north of Tierra del Fuego (Argentina) consisting of two wind turbines alongside a battery system. It’s an installation completely isolated from the grid (off-grid).

The wind farm supplies the Río Cullen and Cañadón Alfa gas treatment plants, which, given their remote location, operate disconnected from the grid, most likely flaring part of the gas they extract.

The turbines are Goldwind GW136-4.2MW, with permanent magnet Direct Drive technology, prepared for the extreme wind regime and the sub-zero temperatures of Patagonia. Goldwind, which has a strong presence in Argentina, has also signed a long-term O&M contract.

An interesting detail is that the batteries, with 9.2 MWh of capacity, are from SAFT, TotalEnergies’ own storage subsidiary. Vertical integration.

Although it has been presented as the world’s southernmost wind farm, the truth is we know there is at least one wind farm in Antarctica as well, so that wouldn’t be entirely accurate. By the way, we talked about that wind farm in edition #131, since it’s going to be repowered.

This project inevitably brings to mind Tropicana, one of the largest off-grid renewable systems in the world, located at AngloGold Ashanti’s Australian mine, combining solar generation with batteries and Goldwind turbines.

And, all things considered, it also recalls Hywind Tampen, where the floating wind turbines power the consumption of an oil platform.

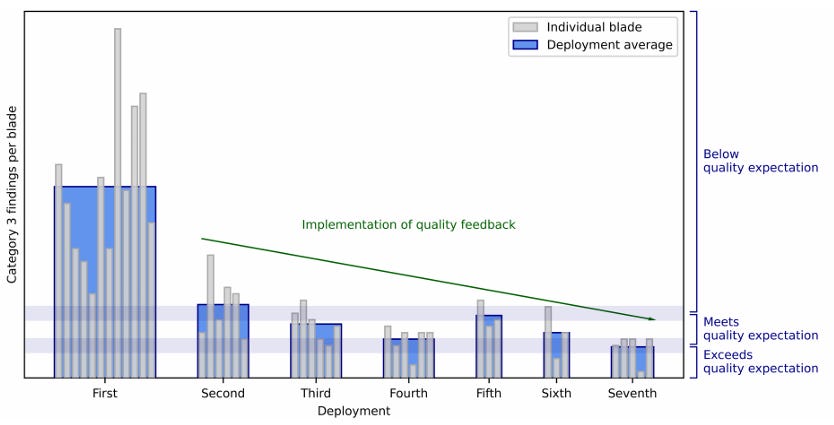

🔍 DNV and GE Vernova collaborate to improve the reliability of onshore blades

Blade reliability is one of the sector’s great challenges in recent years. It’s a truly delicate matter, since the costs of any blade problem skyrocket, especially when we’re talking about catastrophic events, but also about “on site” replacements or repairs.

With the aim of improving its product, GE Vernova has given the certifier DNV access to its blade factories so it can independently audit their quality. The manufacturer is not exactly small in this field: it has 13 blade factories on four continents and in 2023 alone it produced 23,400 blades, reaching some 267,000 over its 47-year history.

According to the technical document published by both companies, DNV reviewed close to 200 blades of 9 different models at 7 of GE Vernova’s own factories (the first one in India). The work consisted mainly of visual inspections of the interior and exterior of already-finished blades, that is, quality control at the factory.

The defects that weigh most heavily (adhesive failures, laminate cracks and poorly executed repairs) are one of the main causes of unplanned downtime, and directly affect production, availability, insurers’ exposure and the developer’s profitability over the entire life of the wind farm. That’s why it’s worth identifying them at the factory and not in the field.

What makes a good blade? According to the inspectors, three things: structural integrity (no critical defects compromising strength), manufacturing consistency (uniformity along the entire blade, without large variations) and surface quality (a good finish that avoids erosion or fatigue problems).

When the project began, one of the ten production lines audited was making blades “below the quality expected by the industry.” According to the report, it’s the one that has improved the most.

GE Vernova arrives at this exercise after a run of highly publicized blade problems, such as those at Vineyard Wind or Dogger Bank, even if they were offshore.

You can read the full report here.

⚓ Dajin wants to offer Europe turnkey monopiles: manufacturing, transport and installation

The Chinese foundations manufacturer Dajin Heavy Industry wants to take a further step in Europe and offer an integrated “one-stop shop” solution that combines manufacturing, transport, marshalling (the storage and pre-assembly at port) and installation in a single package.

The truth is they already have transport experience. Their cargo vessel King One transported the Hornsea 3 monopiles from China to the United Kingdom for Ørsted (2.9 GW).

In Europe, the supply chain is currently fragmented: some manufacture the foundations (Sif, EEW, Steelwind, Navantia-Windar, Haizea), different players own the installation vessels (Cadeler, Van Oord, DEME, Jan De Nul), and the developer contracts each piece separately, on top of the marshalling ports.

That’s where Dajin sees an opportunity. The advantage of its model is clear: a single point of contact, cheaper Chinese steel and, above all, its own vessels that sidestep the shortage suffocating developers. And the drawbacks, you already know them: importing Chinese foundations, transported on Chinese operated vessels and installed by Chinese means, runs head-on into European industrial policy and into the debate about dependence on China for critical infrastructure.

On the other hand, for the floating sector, they have already commissioned the Dutch company Jumbo Marine to build two heavy-lift vessels (two 1,200 t cranes, with a capacity of 2,400 t working in tandem) designed to sink and position floating foundations in Europe, positioning themselves for the project pipeline that is coming.

Thank you very much for reading Windletter and many thanks to Tetrace, RenerCycle, Nabrawind and Ingeteam, our main sponsors, for making it possible.

And if you feel like it, recommend Windletter to help me grow 🚀

See you next time!

Disclaimer: The opinions presented in Windletter are mine and do not necessarily reflect the views of my employer.